RBI Opens M&A Financing:

What

the Numbers Actually Say

After 70 years of prohibition, Indian

banks can now fund corporate acquisitions. Here's a data-first breakdown of the

rules, the market size, and what it means for dealmakers.

Effective Date:

April 1, 2026 · Framework: RBI Capital Market Exposure

Directions, 2026

|

₹5L Cr Estimated lending opportunity unlocked |

70 yrs Duration of the prior prohibition |

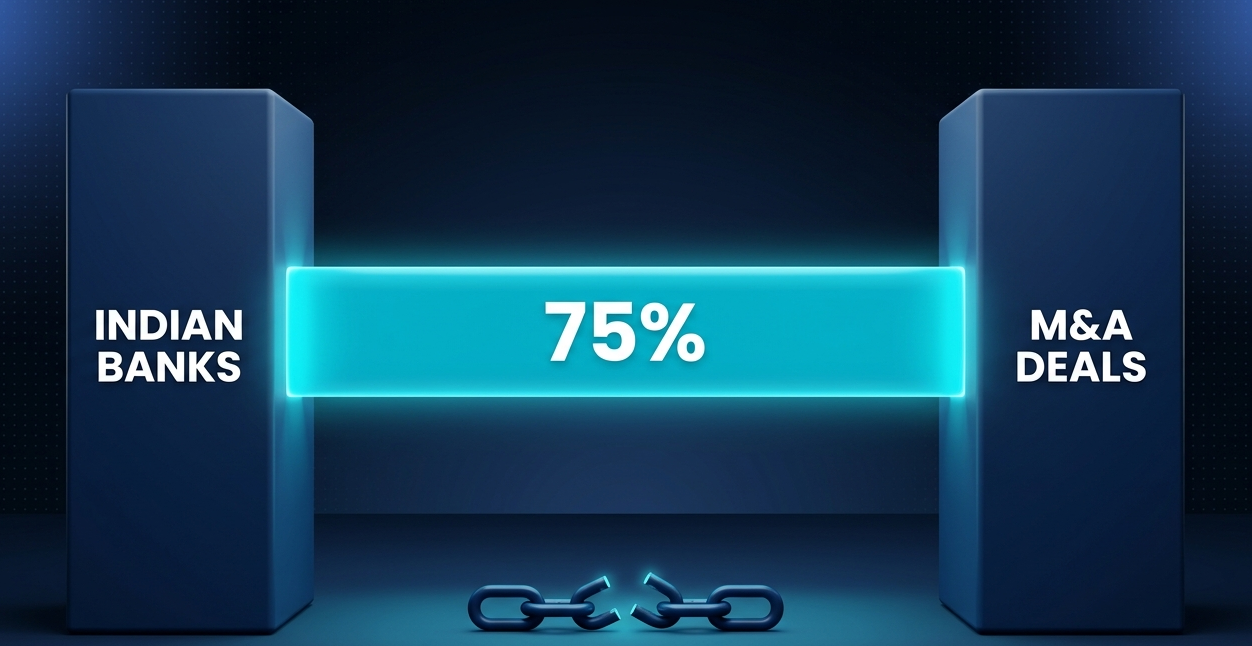

75% Max bank financing of deal value |

20% Cap on Tier-1 capital per bank |

The Rule Change, Precisely

On February 13,

2026, the RBI issued final Amendment Directions under its Capital Market

Exposure framework, effective April 1, 2026. The rules doubled the acquisition

finance cap from the initially proposed 10% to 20% of a bank's Tier-1 capital —

after banks collectively pushed back during the consultation period.

|

PARAMETER |

FINAL

RULE (FEB 2026) |

|

Max bank

financing per deal |

75% of

acquisition value |

|

Min promoter

contribution |

25%

equity, own funds |

|

Acquisition

finance cap per bank |

20% of

Tier-1 capital |

|

Total direct

capital market exposure |

40% of

Tier-1 capital |

|

Borrower

eligibility |

Min ₹500

Cr net worth, 3 yrs profitable, listed |

|

Max

debt-equity of acquirer |

3:1 |

|

Valuation

requirement |

2

independent valuations mandatory |

|

Scope |

Non-financial

entities only; PSU disinvestment allowed |

How Big Is India's M&A Market Right Now?

The policy arrived at a moment

when Indian dealmaking is already accelerating sharply.

|

$157.9B Total deal value, India 2025 Source: LSEG |

$26B M&A value, Jan–Sep 2025 649 transactions · EY India |

+37% YoY growth in M&A value, 2025 vs +10% globally |

+66% India deal surge vs Asia-Pacific APAC declined 5% same period |

Sector-wise in 2025, industrials

led with $35.4B (+221% YoY), followed by energy & power at $28.9B (+190%),

financials at $27B (+152%), and high technology at $19.9B (+100%).

|

Industrials $35.4B +221% YoY |

Energy & Power $28.9B +190% YoY |

|

Financials $27.0B +152% YoY |

High Technology $19.9B +100% YoY |

What Was Broken Before

Indian banks

were categorically banned from financing acquisitions since the 1950s. The

logic: acquisitions involve ownership transfer, not asset creation. Banks were

expected to fund capex and working capital not help one company buy another.

This created a structural gap.

|

Companies needing acquisition capital had to route deals

through NBFCs, foreign banks, or PE firms

all significantly more expensive than domestic bank credit. Management

buyouts (MBOs) and leveraged buyouts (LBOs) were structurally impossible for

most Indian corporates without expensive offshore structures. |

The SBI

chairman in August 2025 publicly said the Indian Banks Association would

formally petition the RBI for this change — a signal of how deep the demand was

within the system. Two months later, the RBI announced the framework.

Timeline of the Reform

▸

OCT 1, 2025 RBI Governor Sanjay Malhotra announces enabling framework for

bank M&A financing in MPC statement.

▸

OCT 24, 2025 Draft RBI (Commercial Banks – Capital Market Exposure)

Directions released for public consultation; proposes 70% deal financing, 10%

Tier-1 cap.

▸

NOV 21, 2025 Deadline for stakeholder comments; banks push for higher Tier-1

cap.

▸

FEB 13, 2026 Final Amendment Directions issued: cap raised to 20% Tier-1,

deal financing to 75%, ₹500 Cr net worth requirement added.

▸

APR 1, 2026 Rules come into force. Banks begin building internal acquisition

finance policies.

What It Means for PE & VC Exits

This is

arguably the highest-impact downstream effect. PE and VC firms in India have

consistently faced a structural problem: finding domestic buyers with cheap

financing. Without bank-backed acquisition loans, buyers relied on expensive

private credit, suppressing bid values and slowing exit timelines.

With banks now

able to finance up to 75% of a deal, a buyer acquiring a ₹1,000 Cr company

needs to bring only ₹250 Cr in equity — the rest can come from a syndicated

bank facility. This directly improves deal economics for both sides and expands

the buyer pool beyond large conglomerates.

|

The 50+

circulars governing capital market exposure since 1986 have been consolidated

and repealed under the new framework — replacing decades of patchwork

regulation with a single unified set of directions. |

The Risk the RBI Is Managing

Experts have

flagged two concerns. First, asset-liability mismatch: acquisition loans tend

to be long-duration (5–7 years) while bank funding is typically shorter.

Second, concentration risk if multiple large deals sour simultaneously.

The 20% Tier-1

cap, the 25% promoter contribution floor, the 3:1 debt-equity limit, and the

requirement for two independent valuations are all explicitly designed to

prevent the balance-sheet stress seen in infrastructure loan cycles. The

restriction to non-financial entities and profitability requirements further

narrow the eligible pool to the more creditworthy end of the market.

Sources

RBI Amendment Directions (Feb 13, 2026) · EY

India Dealtracker Q3 2025 · LSEG Deals Intelligence 2025 ·

Business Standard · Grant Thornton Bharat Dealtracker ·

AngelOne Research · Lexology / AZB & Partners ·

S&R Associates